Person reviewing insurance declarations page at desk

Insurance Declarations Page Guide to Reading Your Policy Coverage

Content

Your insurance declarations page—often called a dec page—is the single-page snapshot of your entire policy. Think of it as the executive summary of your coverage, showing who's insured, what's covered, how much you'll pay, and the limits that apply if you file a claim.

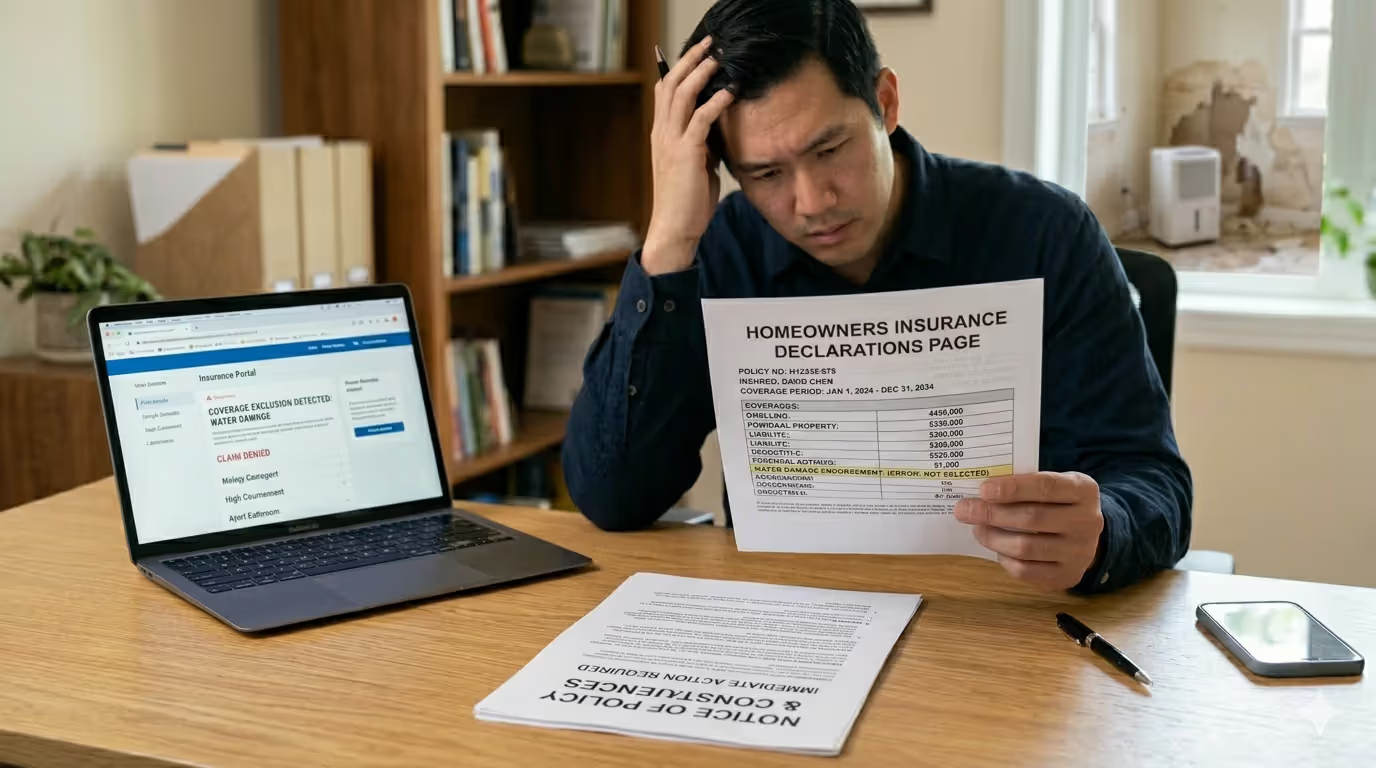

Most policyholders glance at this document once when it arrives, then file it away. That's a mistake. The dec page contains the specific numbers and details that determine whether you're adequately protected or dangerously underinsured. A homeowner who assumes their $250,000 dwelling coverage matches their home's current $400,000 replacement cost might face a six-figure gap after a total loss—all because they never reviewed the coverage limit printed right there on page one.

Every time your policy renews, changes, or gets updated, you receive a fresh declarations page. Understanding how to read this document puts you in control of your insurance program rather than blindly trusting that everything's handled correctly.

I've seen countless claims where policyholders were shocked to learn their actual coverage limits. They'd been paying premiums for years but never verified the numbers on their declarations page matched their real-world needs. That five-minute review can prevent a financial catastrophe.

— Michael Torres

The Core Components of Your Dec Page

Insurance companies use slightly different formats, but every declarations page follows the same basic structure. Here's what you'll find in each section and why it matters.

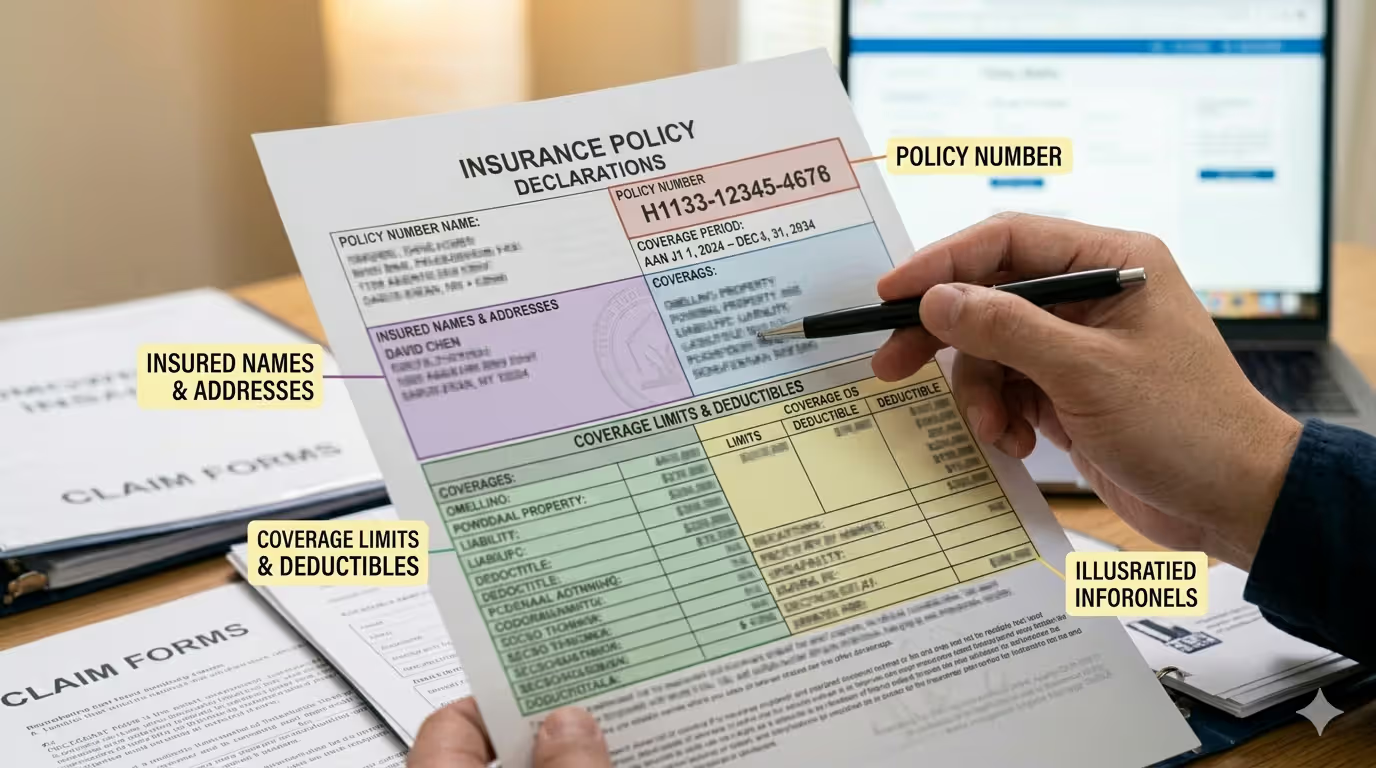

Policy identification and coverage period

The top portion displays your policy number—a unique identifier you'll need for any customer service call, claim, or coverage question. Write this number in your phone contacts or password manager so you can access it quickly.

Right below that, you'll see the policy period: specific start and end dates, typically spanning six or twelve months. Your coverage only applies during this window. If you're in a car accident on March 15 but your policy expired March 1, you have no coverage—even if you thought it renewed automatically.

The policy period also determines which version of your policy applies if the insurance company changes rates or terms. Some carriers adjust coverage or exclusions at renewal. Comparing your current dec page to last year's reveals these changes before they matter.

Named insured and property details

This section lists exactly who's covered and what property the policy protects. For auto insurance, you'll see the vehicle identification number (VIN), year, make, and model for each car. For homeowners insurance, the property address appears along with construction details like square footage or year built.

Pay attention to how names appear. If your policy lists "John Smith" but your spouse drives the car regularly, they might not be covered unless specifically added. Joint property owned by "John Smith and Maria Smith" should show both names as named insureds.

The property description matters more than most people realize. If your dec page lists your home as a "single-family dwelling" but you've converted the basement into a rental unit, you might have no coverage for tenant-related claims. The description on this document must match reality.

Author: Calvin Prescott;

Source: trialstribulations.net

Coverage limits and deductibles

This is where your policy gets real. Every coverage type shows a maximum limit—the most the insurance company will pay for that category of loss. These appear as dollar amounts, sometimes with per-person and per-occurrence distinctions.

Your deductible is the amount you pay out-of-pocket before insurance kicks in. A $1,000 deductible on a $3,500 claim means you receive $2,500. Higher deductibles lower your premium but increase your financial exposure on smaller claims.

Some policies use percentage deductibles for specific perils. A 2% wind/hail deductible on a home insured for $300,000 means you pay the first $6,000 of storm damage. That's substantially different from a flat $1,000 deductible, yet both might appear as simple lines on your coverage details sheet.

How Your Premium Gets Calculated

The premium section shows what you actually pay, broken down into components that explain where your money goes. Understanding this premium breakdown helps you make informed decisions about coverage adjustments.

Your base premium reflects the pure cost of coverage based on your risk profile—your driving record, home's age, credit score, claims history, and dozens of other rating factors. This number comes from actuarial tables that predict how likely you are to file a claim.

Then come the fees and surcharges. You'll often see a policy fee (a flat administrative charge), installment fees if you pay monthly rather than annually, and state-mandated assessments. Some states require insurance companies to contribute to guarantee funds that protect policyholders if an insurer goes bankrupt; those costs get passed along as line items.

Discounts appear as negative numbers or percentage reductions. Multi-policy discounts, claims-free discounts, safety feature credits, and paid-in-full discounts all reduce your total. The dec page shows which discounts you're receiving—and by extension, which ones you're missing.

The final number is your total premium due. For policies with payment plans, you'll see the down payment and installment amounts. Double-check that your actual billing matches these figures. Billing errors happen, and catching them early prevents coverage lapses.

Author: Calvin Prescott;

Source: trialstribulations.net

Coverage Types Listed on Your Declarations Sheet

Insurance policies use abbreviations, codes, and industry shorthand that make perfect sense to underwriters but confuse everyone else. Here's how to decode the coverage types on your policy summary explained in plain language.

Auto policies typically list six main coverage types. Bodily Injury (BI) covers injuries you cause to other people. Property Damage (PD) pays for damage to others' vehicles or property. These are usually shown as split limits like "100/300/100," meaning $100,000 per person for injuries, $300,000 per accident for injuries, and $100,000 for property damage.

Comprehensive (Comp) and Collision (Coll) protect your own vehicle. Collision pays for crash damage regardless of fault; comprehensive covers theft, vandalism, weather, and animal strikes. Medical Payments (Med Pay) or Personal Injury Protection (PIP) covers your own medical bills after an accident.

Homeowners policies organize differently. Dwelling coverage (Coverage A) protects the house structure. Other Structures (Coverage B) covers detached garages or sheds. Personal Property (Coverage C) protects your belongings. Loss of Use (Coverage D) pays for temporary housing if your home becomes uninhabitable. Personal Liability (Coverage E) and Medical Payments to Others (Coverage F) protect you if someone's injured on your property.

| Coverage Line Item | What It Means | Typical Limits |

| Bodily Injury Liability | Injuries you cause to others in an auto accident | $100,000–$500,000 per person |

| Property Damage Liability | Damage to others' property from your vehicle | $50,000–$300,000 per accident |

| Dwelling Coverage | Rebuilding your home's structure after covered loss | Replacement cost value of home |

| Personal Liability | Legal defense and damages if you're sued for injury/damage | $100,000–$500,000 per occurrence |

| Medical Payments | Medical bills for guests injured on your property | $1,000–$5,000 per person |

| Comprehensive | Damage to your car from non-collision events | Actual cash value minus deductible |

| Collision | Damage to your car from crashes regardless of fault | Actual cash value minus deductible |

| Loss of Use | Temporary housing during home repairs | 20%–30% of dwelling coverage |

Endorsements add or modify coverage. These appear as separate line items with their own premiums. An umbrella policy endorsement might add $1 million in liability coverage. A scheduled personal property endorsement lists high-value items like jewelry or art with specific coverage amounts.

Author: Calvin Prescott;

Source: trialstribulations.net

5 Common Mistakes People Make Reading Their Dec Page

Even financially savvy people misinterpret their declarations pages. These errors create coverage gaps that only surface during claims—the worst possible time to discover you're underinsured.

Assuming your limits are adequate because you've had them for years. Insurance needs change. The $250,000 liability limit that seemed generous when you bought your first home might be dangerously low now that you have significant assets to protect. Review your limits annually against your current net worth and replacement costs. Inflation alone can turn adequate coverage into a shortfall.

Ignoring endorsements or not understanding what they do. That "Equipment Breakdown" endorsement on your homeowners policy might be the only thing covering your HVAC system failure. The "Rental Reimbursement" add-on for your auto policy could save you $800 in car rental fees after an accident. Read every endorsement listed and confirm you understand what additional protection you're paying for—or what gaps remain because you declined coverage.

Confusing per-occurrence limits with aggregate limits. A $300,000 per-occurrence liability limit might come with a $600,000 aggregate limit, meaning that's the total the policy will pay across all claims during the policy period. If you have two separate liability claims totaling $400,000 each, you'd face $200,000 in uncovered losses despite each claim being under your per-occurrence limit.

Overlooking named drivers or excluded items. Your teenager might be listed as an excluded driver to reduce premiums, but that means zero coverage if they borrow your car. Similarly, that home-based business you started might be specifically excluded from your homeowners policy. These exclusions appear in small print on your insurance documents guide but carry major consequences.

Missing renewal changes buried in the details. Insurance companies can adjust coverage, limits, deductibles, and terms at renewal. Your wind/hail deductible might jump from $1,000 to 2% of dwelling coverage—a change that could cost you thousands more out-of-pocket. Your liability limits might decrease if the carrier is pulling back in your market. Always compare your new dec page line-by-line against the previous version.

Author: Calvin Prescott;

Source: trialstribulations.net

When You'll Actually Need This Document

Your declarations page sits dormant most of the time, then suddenly becomes essential. Keep both physical and digital copies accessible so you're not frantically searching during an emergency.

Filing a claim requires your policy number and coverage details. Adjusters need to verify your deductible, limits, and effective dates before processing your claim. Having your dec page handy speeds up this process significantly—especially important when you're dealing with property damage or injury stress.

Mortgage and lease requirements often mandate proof of insurance with specific minimum coverage amounts. Lenders want to see that dwelling coverage meets or exceeds the loan amount. Landlords require renters insurance declarations showing liability coverage. You'll submit your dec page to satisfy these requirements.

DMV and vehicle registration in most states requires proof of auto insurance. While some states have electronic verification systems, many still require you to present your declarations page showing current coverage for each vehicle you're registering.

Switching insurance carriers goes smoother when you can show your current coverage details to prospective insurers. They'll match or adjust your coverage based on what's listed on your existing dec page. This prevents gaps or duplications during the transition.

Loan applications and financial transactions sometimes require proof of insurance. Business loans, equipment financing, and even some employment applications ask for evidence of adequate coverage. Your policy info on the declarations page serves as that proof.

Store a photo of your dec page in your phone and keep a paper copy in your home file system—not in your car, where it could be stolen along with your vehicle. Update these copies every time you receive a new declarations page.

How the Dec Page Differs from Your Full Policy

Your full policy document runs 20 to 60 pages of dense legal language defining coverage terms, exclusions, conditions, and procedures. The declarations page distills this into a one-page summary—but it's not a replacement for the complete policy contract.

The dec page tells you what coverage you have and how much. The full policy explains when coverage applies and what's excluded. You might see "$300,000 Personal Liability" on your dec page, but only the full policy reveals that intentional acts, business activities, and certain dog breeds are excluded from that coverage.

Exclusions and limitations don't appear on declarations pages. That's by design—the dec page is a summary, not a contract. If you want to know whether your policy covers foundation cracks, mold damage, or flood losses, you need to read the policy itself or ask your agent. The coverage details sheet won't tell you.

The conditions section of your full policy sets requirements you must meet for coverage to apply. Duties after loss, cooperation clauses, notice requirements, and arbitration provisions all live in the policy document. Violating these conditions can void your coverage even if your dec page shows you're insured.

Policy definitions matter enormously. Words like "occurrence," "insured," "property damage," and "bodily injury" have specific legal meanings defined in your policy. The dec page uses these terms but doesn't define them. Misunderstanding a key definition can lead you to believe you're covered when you're not.

Think of the relationship this way: your declarations page is the nutrition label on a food package, while your full policy is the ingredient list and preparation instructions. Both matter, but they serve different purposes. You need the dec page for quick reference and proof of coverage; you need the full policy to understand exactly what's covered and what's not.

Frequently Asked Questions About Insurance Declaration Pages

Your insurance declarations page deserves more than a quick glance and a trip to the filing cabinet. This single document determines whether your coverage matches your actual needs or leaves you exposed to catastrophic financial loss.

Set a calendar reminder to review your dec page every six months. Compare coverage limits against current replacement costs, verify that all drivers and properties are correctly listed, and confirm your deductibles align with your emergency fund. Check that you're receiving all applicable discounts and that no unexpected changes appeared at renewal.

When life changes—you buy a home, have a child, start a business, acquire valuable property—pull out your declarations page and assess whether your coverage still fits. Insurance needs evolve, but policies don't update automatically.

The five minutes you spend understanding your policy info today could save you five figures in uncovered losses tomorrow. Your declarations page isn't just paperwork—it's a financial tool that works only if you know how to read it.