Person with new SUV at dealership after purchase

Gap Insurance Guide to Coverage Costs and When You Need It

Content

You drive your brand-new car home—$35,000 SUV, financed with maybe $2,000 down. Feels amazing, right? Here's what the dealer won't mention during that celebration: your vehicle just dropped to $28,000 in market value. Literally as you pulled onto the highway. Six months pass, someone T-bones you at an intersection, and the insurance adjuster totals your SUV. Your carrier cuts a check for $28,000 (current market value), but you still owe $33,000 on the loan. That $5,000 difference? You're paying it out of pocket for a vehicle sitting in a salvage yard. This nightmare scenario is precisely why gap coverage exists—though figuring out if you actually need it, or if you're throwing money at unnecessary protection, confuses most buyers.

What Is Gap Insurance and How Does It Work?

This coverage—Guaranteed Asset Protection in industry speak—handles the financial shortfall when your loan balance exceeds your vehicle's market value after a total loss. Your standard collision and comprehensive policies? They pay current market value only, completely ignoring whatever you still owe the bank.

Author: Brandon Whitaker;

Source: trialstribulations.net

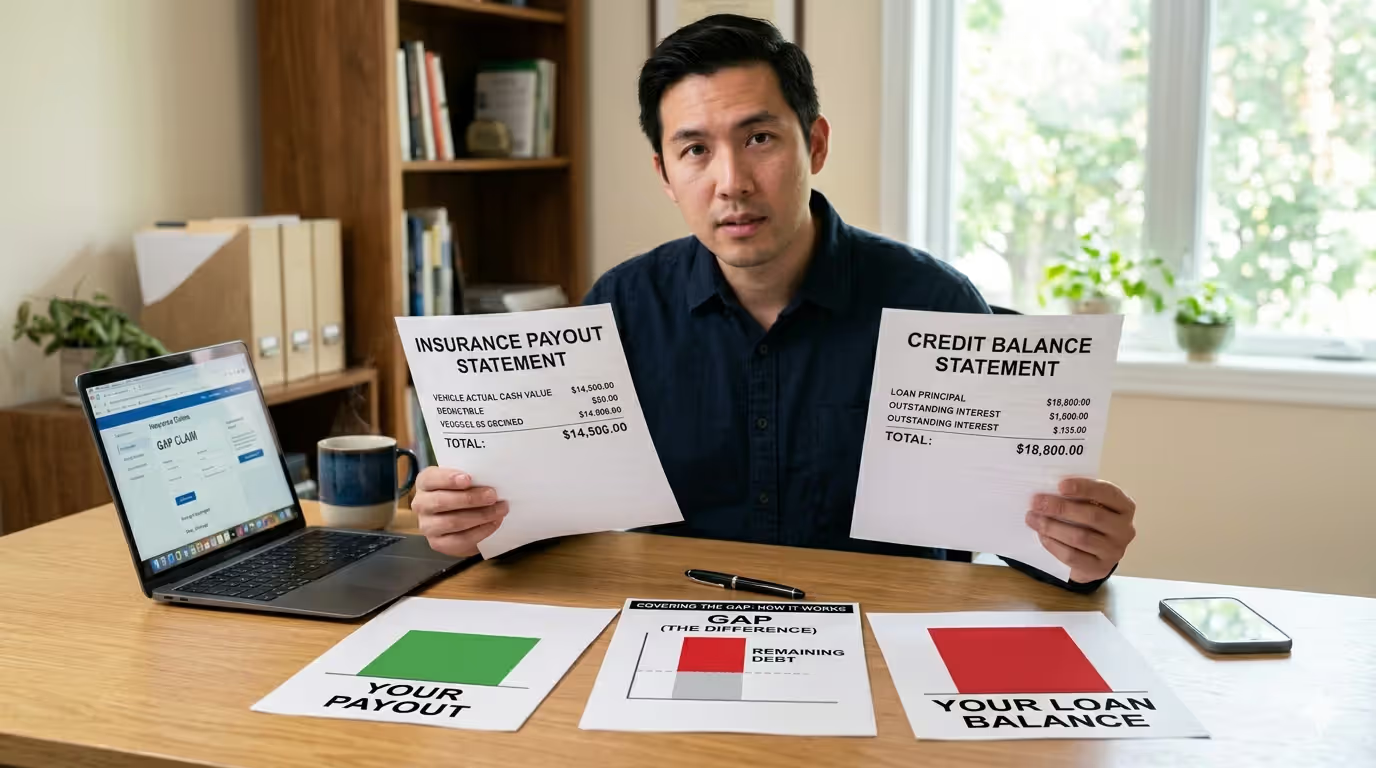

Let's walk through an actual claim scenario. Sarah buys a $32,000 sedan, puts down $2,000, and finances the remaining $30,000 over 72 months at 6%. Eight months in, someone runs a red light and destroys her car. The insurance company's assessment: market value sits at $26,500. Her remaining loan obligation: $28,800. Without gap protection, Sarah writes a $2,300 check to her lender while simultaneously shopping for another vehicle. With coverage, that $2,300 disappears—the gap policy sends payment directly to her bank.

Here's the payment sequence: Your primary auto insurance settles first, paying whatever they've determined as fair market value. Then your gap provider steps in, covering the difference between that payout and your actual loan payoff amount. Most policies cap this at 25% of the vehicle's assessed value. Many also handle your deductible—typically up to $1,000—so you're not covering that out-of-pocket either after losing your vehicle.

Expert Perspective:

Here's what I've noticed after nearly two decades in auto finance consulting. People assume gap coverage is just dealers padding their profits—and honestly, that happens constantly. But the protection itself? Absolutely legitimate for specific situations. What really bothers me is the pricing games. I've reviewed contracts where dealerships charged $995 for gap policies available through Geico or State Farm for $35 annually. We're talking 400% markups. The second issue—and this costs consumers thousands—is keeping these policies active way too long. Most drivers only face negative equity risk during the first 24-36 months. After that, your loan balance typically drops below the vehicle's worth. Yet I see people paying for gap protection through year six of a loan when they've had equity since year three. Check your loan balance against your car's value every twelve months. Once those numbers flip and you owe less than it's worth, cancel immediately and pocket the refund.

— Marcus Chen

When Gap Insurance Makes Financial Sense

This totaled car insurance protection isn't universal. Plenty of buyers waste money on unnecessary coverage.

New vehicles hemorrhage value fastest during years one through three. First-year depreciation often hits 20%, second year drops another 15%. Finance 90% of the purchase price or more? You're underwater immediately and stay there for years. Stretch that loan to 72 or 84 months, and you might carry negative equity for four years straight.

Leased vehicles create different math. You're financing the depreciation portion specifically, which means negative equity is essentially guaranteed throughout the lease term. Check your lease paperwork—most manufacturers bundle gap protection automatically, though some charge separately for this leasing insurance guide component.

Rolling underwater debt from your trade-in creates massive gaps instantly. Owe $4,000 more than your old car's worth, and the dealer rolls that into your new loan? You start owing $4,000 beyond the new vehicle's value before adding normal depreciation.

Author: Brandon Whitaker;

Source: trialstribulations.net

High-Risk Scenarios for Negative Equity

Certain financing structures virtually guarantee multi-year negative equity requiring this negative equity insurance:

Nothing down: Zero down payment means zero equity cushion. A $40,000 vehicle worth $34,000 three months later, with you owing the full $40,000 plus accruing interest.

84-month payment plans: You're still paying mostly interest during year three of a seven-year loan. Meanwhile the vehicle keeps depreciating. Principal barely budges while market value plummets.

Interest rates exceeding 8%: More of your monthly payment feeds interest instead of reducing what you owe. Combine that with steady depreciation and the gap widens rather than shrinks.

Luxury models and EVs: Some vehicles lose value faster than typical. Electric vehicles can drop 30-40% in year one as battery technology advances and federal tax credits only apply to new purchases.

Leasing vs. Financing Considerations

Lease contracts typically include built-in gap protection, but verify before signing anything. Toyota and Honda bundle it standard. Other manufacturers treat it as an add-on fee. For financed purchases, the decision falls entirely on you.

Putting 20% down on a 48-month loan? You probably don't need coverage—you're building equity faster than depreciation erodes value. But minimal down payment with extended terms? That's when finance protection becomes essential, especially with today's inflated vehicle prices pushing buyers toward longer loans.

What Gap Insurance Actually Covers (And What It Doesn't)

These policies handle the dollar difference between market value and loan payoff when your vehicle is declared a total loss, plus deductibles in most cases. Coverage kicks in for:

- Collision damage resulting in total loss

- Stolen vehicles never recovered

- Fire destroying the vehicle

- Flood or severe weather damage

- Vandalism causing total loss

Most policies absorb your primary insurance deductible—up to $1,000—preventing that expense from hitting you after a total loss.

Coverage exclusions you need to know:

Mechanical breakdowns don't qualify. Transmission fails completely? You're still making full loan payments with no insurance assistance.

Late payment penalties and missed payment balances aren't covered. The policy addresses the gap between market value and your original loan amount—not fees you've accumulated through delinquency.

Extended warranties, service contracts, and credit insurance bundled into your financing don't receive gap coverage. Only the vehicle's actual financed cost counts.

Excessive negative equity rolled from previous loans may face coverage caps. Some policies limit how much previous-loan debt they'll protect.

Death or disability coverage remains separate. Dealers sometimes package credit life insurance alongside gap protection, but they're completely different products serving different purposes.

Where to Buy Gap Insurance and What It Costs

Three main sources offer loan payoff coverage with dramatically different pricing and terms.

Dealerships handle everything at purchase, rolling the cost into your auto loan. Ultimate convenience, maximum expense—dealers typically charge $500-995 as a single fee. That amount gets financed with your vehicle, meaning you'll pay interest on the insurance premium throughout your entire loan term.

Auto insurance companies add gap coverage to your existing policy for $20-60 yearly. You'll pay monthly or in one annual chunk, can cancel whenever you want, and avoid financing the insurance cost. State Farm, Geico, Progressive, and Allstate all offer this option.

Banks and credit unions selling you the auto loan often provide gap insurance for $200-400 as a single payment or $15-40 annually. Credit unions frequently beat other sources on member pricing.

Author: Brandon Whitaker;

Source: trialstribulations.net

Gap Insurance Provider Comparison

| Provider Type | Average Cost | Payment Method | Cancellation/Refund | Best For |

| Dealership | $500-$995 single charge | Added to your loan amount | Prorated refund available if you cancel early; expect paperwork hassles | Buyers wanting everything finished at signing despite paying premium prices |

| Auto Insurance Company | $20-$60 per year | Monthly premium or annual payment | Cancel anytime with no refund complications | Budget-conscious buyers who can shop rates yearly and want flexibility |

| Bank/Credit Union | $200-$400 single charge or $15-$40 annually | Paid upfront or added to loan | Prorated refunds available; simpler process than dealerships | Members seeking competitive pricing with institutional reliability |

The math reveals serious differences. A $700 dealer policy financed at 6% over six years actually costs you $850 after interest. That identical coverage through Progressive might run $180 total across three years—saving you $670.

How to Calculate If You Have a Coverage Gap

Determining your need for finance protection requires three numbers: current loan payoff, vehicle's actual cash value, and the difference.

Step 1: Get your exact loan payoff amount. Log into your lender's online portal or call them directly for a payoff quote. This includes remaining principal, interest that's accrued, and any applicable fees. Don't rely on last month's statement balance—get today's actual payoff figure.

Step 2: Determine your vehicle's current market value. Use multiple sources because estimates vary: - Kelley Blue Book (kbb.com)—select "fair" condition since insurance companies use conservative estimates - NADA Guides (nadaguides.com)—reference "clean trade-in" value - Edmunds (edmunds.com)—check their "True Market Value" tool

Average these three estimates. Insurance adjusters typically land on the lower end, so conservative estimates match reality better.

Step 3: Do the subtraction. Take your loan payoff and subtract market value. Positive number (you owe more than it's worth)? That's your gap. Negative number means you have equity and don't need coverage.

Example calculation: Your loan payoff is $24,600. Market value averages $22,800 across the three sources. Your gap measures $1,800.

Step 4: Repeat this calculation every six to twelve months. As you chip away at your loan and your vehicle's depreciation slows, that gap shrinks. Once you flip to equity territory—owing less than the car's worth—cancel your coverage immediately to stop wasting money.

Most drivers only need this protection for 24-36 months maximum. Maintaining it longer means paying premiums for a situation that can't happen.

Alternatives to Gap Insurance for Loan Payoff Protection

Several approaches reduce or completely eliminate the need for coverage.

New car replacement coverage from select insurers pays to replace your totaled vehicle with a brand-new equivalent model rather than cutting a check for depreciated value. Available for vehicles under one year old, this protection costs more than gap insurance but delivers better results. Liberty Mutual, Nationwide, and The Hartford offer versions.

Substantial down payments create instant equity buffering you against depreciation. Put 20% down, and you'll likely never need gap coverage. A $6,000 down payment on a $30,000 vehicle means you start with equity even as the car loses value.

Shorter loan terms build equity faster than depreciation can erase it. A 36-48 month loan keeps your principal payments high relative to the balance, closing any gap quickly. Monthly payments increase, sure, but you'll pay drastically less interest overall and need gap coverage briefly if at all.

Superior loan terms through credit unions or manufacturer incentives often deliver lower interest rates. Less interest means more of each payment attacks principal, building equity faster. A 3.9% rate versus 7.9% might eliminate gap insurance need entirely on an identical vehicle.

Certified pre-owned purchases have already absorbed the steepest depreciation. A two-year-old CPO vehicle with 25,000 miles has weathered most value loss. Finance 80-90% of that purchase, and you're unlikely to face negative equity.

Author: Brandon Whitaker;

Source: trialstribulations.net

Common Mistakes When Buying or Skipping Gap Coverage

Purchasing from the dealer without checking other prices. Dealers mark up gap coverage substantially because most buyers don't realize they have options. Always contact your auto insurance company before agreeing to dealer coverage. You'll save hundreds, possibly more.

Maintaining coverage throughout your entire loan term. Once you've built equity—usually after 2-3 years—you're funding coverage you cannot possibly use. Review your loan-to-value ratio every twelve months and cancel when you've crossed into equity territory.

Believing comprehensive and collision insurance covers this gap. Standard policies pay market value only, never your loan balance. This misconception leaves people stunned after a total loss when they discover they're writing a five-figure check for a car in the junkyard.

Skipping coverage despite minimal down payment and 72+ month loans. This combination guarantees years of negative equity. One accident or theft, and you're paying off nothing for years.

Ignoring cancellation rights and refund provisions. Most gap policies offer prorated refunds when you cancel early—whether from paying off the loan, selling the vehicle, or building sufficient equity. Dealer policies often bury refund provisions in contract fine print. Refinance or pay off early? File for that refund.

Buying protection when you've put substantial money down. Drop 25-30% on a vehicle that holds value well, and this coverage is unnecessary. You're paying premiums for a problem that won't materialize.

Forgetting to notify your gap provider after a total loss. Gap insurance doesn't trigger automatically. After your primary insurance settles, you must file a separate claim with your gap provider, submitting their settlement documentation and your loan payoff statement. Skip this step despite having coverage? You'll pay that gap yourself.

Frequently Asked Questions About Gap Insurance

Gap insurance serves one specific purpose: protecting borrowers from negative equity following a total loss. The coverage makes financial sense when you're financing most of a vehicle's cost with minimal down payment and extended loan terms—situations creating years of owing more than the car's worth. Leased vehicles almost always benefit from this protection.

The critical factors are buying coverage at the right price from the right source. Dealer gap insurance costs three to five times more than identical coverage from your auto insurance company. That $700 dealer policy might cost $40 yearly through your insurer—a difference of several hundred dollars across the coverage period.

Equally important: knowing when to cancel. Most people need gap coverage for 2-3 years maximum. Once you've built equity through regular payments and your vehicle's value stabilizes, you're paying premiums for protection you physically cannot use. Check your loan-to-value ratio every twelve months and cancel when the numbers flip.

For buyers putting 20% or more down with loan terms under 60 months, gap insurance often isn't necessary. You build equity faster than depreciation creates gaps. For everyone else—especially those financing 90%+ over 72 months—gap coverage prevents financial catastrophe if the worst happens. Just make certain you're not overpaying for that peace of mind.