Driver reviewing car damage after accident with insurance context

Car Insurance Deductible Guide to Choosing the Right Amount

Content

Your car insurance deductible determines how much you'll pay out-of-pocket before your insurer covers the rest of a claim. For most drivers, this single number shapes both monthly premium costs and financial exposure after an accident. Understanding how deductibles work—and choosing the right amount—can save you hundreds of dollars annually while protecting you from unmanageable repair bills.

What Is a Deductible and When Do You Pay It?

A deductible in car insurance is the dollar amount you agree to pay toward covered repairs or replacement before your insurance company pays the remaining balance. You select this amount when purchasing your policy, typically ranging from $250 to $2,000.

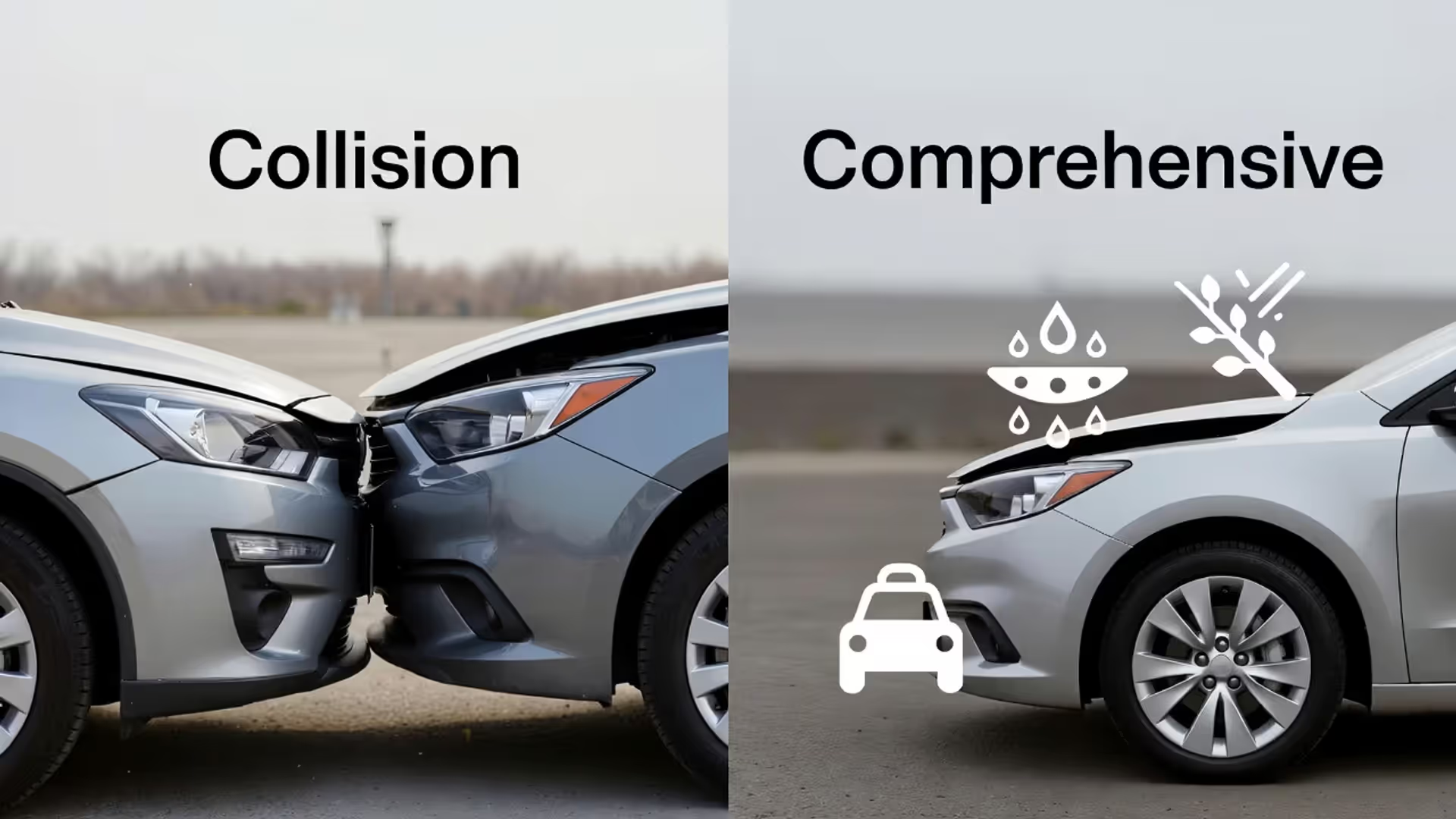

Deductibles apply only to collision and comprehensive coverage—the portions of your policy that protect your own vehicle. Collision coverage handles damage from accidents with other vehicles or objects, while comprehensive covers non-collision events like theft, vandalism, hail damage, or hitting a deer. Each coverage type carries its own deductible, which you can set independently.

Liability coverage operates differently. When you're at fault and damage someone else's property or injure another person, liability coverage pays the claim without requiring a deductible from you. The other driver files through their own collision coverage (and pays their deductible) or through your liability coverage (no deductible for either party).

You pay your deductible when filing a claim for damage to your vehicle. If a tree falls on your car causing $4,500 in damage and you carry a $500 comprehensive deductible, you pay $500 to the repair shop and your insurer covers the remaining $4,000. The deductible applies per claim, not per year—file three claims in twelve months, and you'll pay three separate deductibles.

Author: Calvin Prescott;

Source: trialstribulations.net

How Deductible Amounts Impact Your Premium

Insurance companies use deductibles to share risk with policyholders. Higher deductibles mean you're assuming more financial responsibility for potential claims, which reduces the insurer's exposure. In exchange, they charge lower premiums.

This inverse relationship between deductible and premium follows predictable patterns. Doubling your deductible from $500 to $1,000 typically reduces your collision and comprehensive premiums by 15–30% combined. Quadrupling it to $2,000 can cut those premiums by 30–50%. The exact savings depend on your location, vehicle, driving record, and insurer.

Insurers calculate these differences based on claim frequency data. Most drivers file a collision or comprehensive claim every 10–15 years on average. By choosing a higher deductible, you're betting you'll remain claim-free long enough for premium savings to exceed the additional out-of-pocket cost you'd face in a claim. Insurance companies price deductibles to make this gamble roughly break-even over time, then adjust rates based on their profit margins and competitive positioning.

Real Cost Comparison: $500 vs. $1,000 vs. $2,000 Deductibles

Premium differences become clearer with specific numbers. A 35-year-old driver in Ohio with a clean record insuring a 2020 Honda Accord might see these annual costs:

| Deductible Amount | Annual Premium | Annual Savings vs. $250 | Out-of-Pocket (One Claim) | Break-Even Point |

| $250 | $1,240 | $0 | $250 | — |

| $500 | $1,090 | $150 | $500 | 1.7 years claim-free |

| $1,000 | $940 | $300 | $1,000 | 2.5 years claim-free |

| $2,000 | $780 | $460 | $2,000 | 3.8 years claim-free |

These figures represent combined collision and comprehensive coverage on a policy with $500,000 liability limits. Your actual numbers will vary significantly based on dozens of rating factors, but the proportional relationships hold true across most markets.

Author: Calvin Prescott;

Source: trialstribulations.net

Break-Even Analysis for Premium Savings

The break-even calculation answers a critical question: how many claim-free years do you need for premium savings to offset the higher deductible?

Take the $1,000 deductible example above. You save $300 annually compared to the $500 deductible, but you'd pay an extra $500 out-of-pocket if you file a claim ($1,000 deductible minus $500 deductible). Divide the additional exposure ($500) by annual savings ($300) to get 1.67 years. Stay claim-free for at least 20 months, and you come out ahead even if you then file a claim.

The math shifts for different deductible jumps. Moving from $500 to $2,000 saves roughly $310 per year in this example but increases your exposure by $1,500. Break-even takes nearly five years. If you file a claim in year three, you've saved $930 in premiums but pay $1,500 more out-of-pocket—a net loss of $570.

Most drivers overestimate their claim frequency. If you haven't filed a collision or comprehensive claim in the past decade and maintain good driving habits, higher deductibles usually deliver long-term savings. Drivers with recent claims or high-risk factors (long commutes, urban parking, teenage drivers) should weigh the numbers more carefully.

Choosing Between Low and High Deductibles: What Works for Your Situation

The right deductible balances affordable premiums with manageable financial risk. Four factors should guide your decision.

Author: Calvin Prescott;

Source: trialstribulations.net

Emergency fund status matters most. Can you comfortably pay your deductible tomorrow without using credit cards or depleting savings you need for other emergencies? If a $1,000 unexpected expense would strain your finances, a $1,000 deductible creates real risk regardless of premium savings. Choose the highest deductible you can afford to pay immediately without financial hardship. For many households, that's $500 to $1,000.

Driving history predicts future claims better than most drivers admit. If you've filed two claims in five years, you're statistically more likely to file again than someone with a decade of claim-free driving. Frequent claims make low deductibles more valuable because you'll actually use them. One fender-bender every three years quickly erases any premium savings from a high deductible. Conversely, drivers with spotless records benefit most from maximizing their deductible.

Vehicle value sets an upper boundary. Carrying a $2,000 deductible on a car worth $4,000 makes little sense. If you total the vehicle, you'd receive roughly $2,000 after the deductible—barely worth filing a claim. A useful rule: keep your deductible below 10% of your vehicle's actual cash value. For a $15,000 car, $1,500 represents a reasonable maximum. As your car ages and depreciates, increase your deductible or drop collision and comprehensive coverage entirely.

Claim frequency patterns vary by coverage type. Comprehensive claims (theft, weather, animal strikes) happen more often than collision claims in many areas. Some drivers choose a higher collision deductible ($1,000) paired with a lower comprehensive deductible ($250) because comprehensive coverage costs less and certain risks feel less controllable. This split approach offers flexibility, though it adds complexity.

According to Sarah Mitchell, a licensed insurance agent with 18 years of experience at Midwest Insurance Partners:

I tell clients to choose a deductible that won't keep them awake at night worrying about repair costs, but high enough that they're not tempted to file small claims. The sweet spot for most middle-income families is $500 to $1,000. You want insurance for genuine financial disasters, not routine maintenance disguised as claims.

— Sarah Mitchell

How Deductibles Work in Actual Claims: Payout Examples

Walking through real scenarios clarifies how deductibles affect what you receive from your insurer.

Scenario 1: Minor parking lot collision. You back into a concrete pillar, cracking your bumper and denting the hatch. Repair estimate: $1,400. With a $500 deductible, your insurer pays $900 and you pay $500. With a $1,000 deductible, your insurer pays $400 and you pay $1,000. With a $2,000 deductible, you pay the entire $1,400 out-of-pocket because the damage falls below your deductible—filing a claim makes no financial sense.

Scenario 2: Significant accident damage. You slide on ice and hit a guardrail, damaging the front end, suspension, and airbags. Repair estimate: $8,200. With a $500 deductible, you pay $500 and your insurer pays $7,700. With a $1,000 deductible, you pay $1,000 and your insurer pays $7,200. With a $2,000 deductible, you pay $2,000 and your insurer pays $6,200. The deductible difference matters, but insurance still covers most costs.

Scenario 3: Total loss. A hailstorm totals your vehicle. Your insurer determines the actual cash value at $14,500. With a $500 deductible, you receive $14,000. With a $1,000 deductible, you receive $13,500. With a $2,000 deductible, you receive $12,500. The $1,500 difference between low and high deductibles represents real money, but you're still receiving substantial compensation.

Scenario 4: Comprehensive claim below deductible. Someone keys your car, causing $380 in paint repair costs. Regardless of your deductible amount, filing this claim costs more than you'd receive. You pay the full repair cost yourself. Higher deductibles don't hurt you here because even a $250 deductible wouldn't make this claim worthwhile once you factor in potential rate increases.

These examples illustrate an important principle: deductibles matter most for mid-range claims between $1,000 and $5,000. Very small damage isn't worth claiming regardless of your deductible. Very large damage is catastrophic whether your deductible is $500 or $2,000. The middle ground is where deductible choice significantly affects your out-of-pocket costs.

Author: Calvin Prescott;

Source: trialstribulations.net

Common Deductible Mistakes That Cost Drivers Money

Selecting a deductible you can't actually afford. Chasing premium savings by choosing a $2,000 deductible sounds smart until you cause $3,500 in damage and don't have $2,000 available. Some drivers then skip necessary repairs, drive unsafe vehicles, or pay high-interest credit card charges—outcomes that negate any premium savings. Your deductible should reflect your liquid savings, not your wishful thinking.

Forgetting deductibles apply per claim, not per year. Some drivers mistakenly believe they pay one annual deductible that covers all claims. File three separate claims, and you'll pay three separate deductibles. This misunderstanding leads to poor claims decisions, like filing multiple small claims that each trigger a deductible payment plus potential rate increases.

Never reassessing deductibles as circumstances change. The deductible that made sense when you financed a new car may not fit five years later when you own the vehicle outright and it's worth half the original value. Annual policy reviews should include deductible adjustments. As your emergency fund grows or your vehicle depreciates, increasing your deductible captures premium savings without increasing real risk.

Misunderstanding "disappearing" or "vanishing" deductibles. Some insurers offer programs that reduce your deductible by $50 or $100 for each claim-free year, eventually reaching $0. This sounds appealing but often costs more in additional premium than the deductible reduction is worth. Run the numbers carefully. A standard $500 deductible with lower premiums usually beats a vanishing deductible program for safe drivers.

Ignoring the deductible-premium relationship when comparing quotes. Comparing insurers requires matching deductibles. One company's quote with a $500 deductible can't be fairly compared to another's quote with a $1,000 deductible. Always request quotes with identical deductibles across all insurers, then adjust your chosen deductible after selecting your insurer based on total cost and coverage quality.

Smart Strategies to Save Money on Deductibles and Premiums

Build and maintain a dedicated insurance deductible fund. Open a separate savings account and deposit the monthly premium savings from choosing a higher deductible. If you save $25 monthly by increasing your deductible from $500 to $1,000, deposit that $25 into your deductible fund. Within two years, you've accumulated $600—enough to cover most of the higher deductible if you file a claim. This approach lets you capture premium savings while building a safety net.

Adjust your deductible as your vehicle depreciates. New cars justify lower deductibles because potential claim payouts are substantial. As vehicles age, their value drops while repair costs remain relatively stable. When your car's value falls below $5,000, consider increasing your deductible to $1,000 or dropping collision and comprehensive coverage entirely. The premium savings often exceed the realistic benefit you'd receive from a claim.

Bundle policies to offset deductible costs. Combining auto and homeowners or renters insurance with one company typically saves 15–25% on premiums. Use those savings to afford a lower deductible if you prefer reduced exposure, or pocket the savings while maintaining a higher deductible. Bundling discounts provide flexibility in how you balance premiums and deductibles.

Leverage safe driver programs and telematics. Usage-based insurance programs monitor your driving through smartphone apps or plug-in devices. Safe drivers can earn 20–30% discounts, which creates room in your budget for lower deductibles or simply reduces your total insurance cost. These programs reward the same behaviors that reduce claim frequency, making them particularly valuable for drivers committed to avoiding accidents.

Know when to skip comprehensive coverage entirely. Once your vehicle's value drops below $3,000, comprehensive coverage often costs more over several years than you'd receive from a total loss claim. If you can afford to replace a low-value vehicle out-of-pocket, dropping comprehensive coverage (and its deductible) saves money. Keep liability coverage—that protects you from potentially unlimited financial exposure—but consider self-insuring your older vehicle's physical damage.

Time deductible changes strategically. Most insurers allow mid-policy deductible adjustments, but changes typically take effect on your next renewal. If you're approaching winter in a high-risk climate or planning a long road trip, temporarily lowering your deductible might make sense. Conversely, if you're parking a vehicle for several months, increasing the deductible or suspending collision coverage reduces costs during low-risk periods.

Frequently Asked Questions About Car Insurance Deductibles

Your car insurance deductible represents a fundamental financial trade-off: pay more now in premiums for less exposure later, or pay less now and accept higher out-of-pocket costs if you file a claim. Neither choice is universally correct.

The optimal deductible matches your financial capacity, risk tolerance, and realistic claim likelihood. Drivers with strong emergency funds, clean driving records, and older vehicles benefit most from high deductibles, capturing hundreds in annual savings with minimal downside. Those with tight budgets, recent claims, or high-value vehicles often find lower deductibles provide better peace of mind and protection.

Review your deductible annually as your circumstances evolve. The $500 deductible that fit your situation three years ago might cost you money today if your financial position has strengthened or your vehicle has depreciated. Small adjustments compound over time—increasing a deductible from $500 to $1,000 and pocketing $250 in annual savings delivers $2,500 over a decade, enough to cover five claims at the higher deductible.

Insurance exists to protect you from financial catastrophes you can't absorb on your own. Your deductible defines where your self-insurance ends and your policy's protection begins. Set that line thoughtfully, and you'll pay less for coverage while maintaining the protection you actually need.